Let's start with a small real-life routine. It’s the 7th of the month. You’re wrapping up work around 6:00 PM, feeling the grind of the week, when your phone dings.

A notification flashes: ₹54,000 Salary Credited.

For a few hours, you feel like a king. You’ve worked hard, navigated the office politics, and finally, your bank balance looks respectable. You head home, grab dinner, and go to sleep with a smile, dreaming of that weekend getaway or the new sneakers in your cart.

Then you wake up.

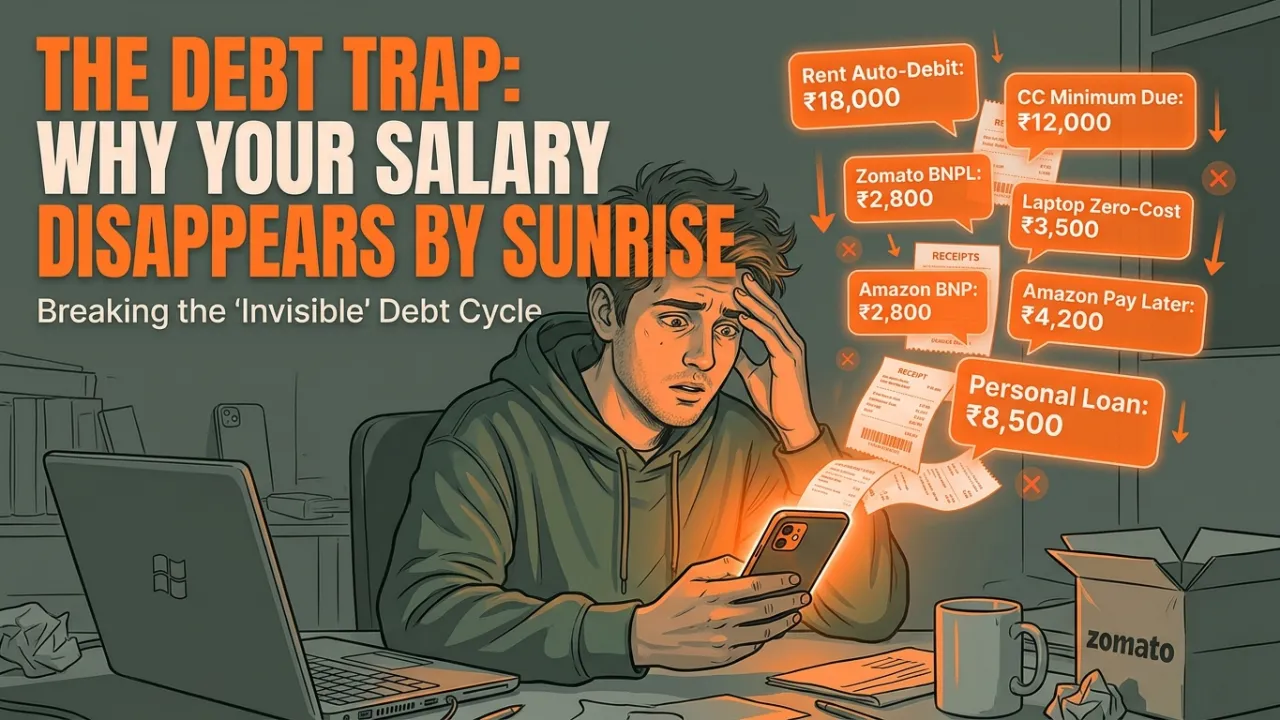

Your phone is a graveyard of transaction alerts. Before you’ve even had your morning tea, the "Invisible Script" has already emptied your pockets:

Rent: ₹18,000 (Auto-debited)

Credit Card Bill: ₹12,000 (Just the 'minimum'—or so you thought)

Laptop Zero-Cost EMI: ₹3,500

Amazon Pay Later: ₹4,200 (For those "deals" last month)

LazyPay/BNPL: ₹2,800 (The "small" food orders that added up)

Personal Loan EMI: ₹8,500 (For that wedding or trip you couldn't afford)

Misc Subscriptions: ₹900

By 8:00 AM, your ₹54,000 has shrunk to barely ₹4,100. The month hasn’t even started, and you haven't bought a single meal for the day yet.

This is not just your story; it's every single person's story in today's modern age.

Let's talk about the real truth: This isn’t a budget problem; it’s a predatory business model.

You are being tricked into living a life that isn't yours, and it’s time to wake up.

1. The "Tap-Tap" Scam: Debt is the New UPI

Back in the days, taking a loan meant sitting before a stern banker and signing fifty documents. Today, you don't "take" a loan; you just "click" a button. Whether it's a ₹499 lunch-feast meal on "Pay Later" or a smartphone on "Zero-Cost EMI," these are unsecured loans hitting your credit history.

Because there’s no physical paperwork, it doesn’t feel like debt - it feels like a convenience. But remember: "A gold-plated cage is still a cage." Banks are spending billions to convince you that "You Deserve This," just so they can lend you your own money back at 36% to 48% interest.

2. The "Minimum Amount Due" Scam

Many of you treat your credit card like a "cashback tool," which is great if you pay the full bill, but if not, think again. Credit card interest isn't 10% or 12%; it’s often 36% to 48%. If you have a ₹1 lakh bill and only pay the Minimum Amount Due, do you know how long it takes to clear? 21 years. You’ll be paying for today’s party well into your middle age.

3. The Hidden Cost: Your Career is at Risk

This is where the "spice" turns into a burn. Most Gen Z professionals don't realize that their "small" ₹2,800 EMI default from three years ago can haunt them today.

The Job Trap: Many companies now run CIBIL background checks. You could lose a high-paying job offer not because you lack skills, but because you missed three EMIs on a gadget years ago. Employers see a "defaulter" and see a liability.

The ₹18 Lakh Penalty: A poor credit score can hike your future home loan interest by just 1%. On a ₹60 lakh loan, that tiny 1% difference costs you an extra ₹15 to ₹18 lakhs over 20 years.

4. Living for the "Gram" (The Ultimate Debt Trap)

Current age generation is obsessed with "Travel Now, Pay Later." A 26-year-old takes a ₹2.5 lakh loan to pose at the Eiffel Tower so they don't look "poor" on Instagram.

Powerful Truth: You are spending money you haven't earned to buy things you don't need to impress strangers who don't care, using a loan that will keep you a "slave" to a job you hate.

Here is a Roadmap on "How to Defy the Faulty Personal Finance Script."

If you want to stop being a "monetization event" for banks, you must change your mindset:

Stop the "Pay Later" Addiction: If you can't buy it twice in cash, you can't afford it. Period.

The Android/Windows Pride: Stop being ashamed of using a 2-generation-old phone or a Windows laptop. Real success is a healthy bank balance, not a titanium-frame phone held by a person with a ₹400 bank balance.

Build a "Risk Fund": Debt keeps you in a toxic job because you have to pay the EMI. Savings give you the power to say "I quit" and take a risk.

Discipline is the Only Currency: Start a small SIP. Not for the returns, but to prove to yourself that you control your money, not the apps (Zomato, Amazon, Myntra Etc) on your phone.

Final Thought: The world wants you in debt so you stay a "mulazim" (an employee/servant) who never dares to dream bigger. Break the cage.

Use the Android, drive the smaller car, and keep your salary in your pocket on the 10th of the month.

Stay disciplined, stay wise.

#FinanceTips #Finance #Investmetn #AmazonPayLater #Paylater #BuyNow #FinancialHelp #MoneyMindset #GenZFinance #PersonalFinanceIndia #FinancialFreedom #FinanceGurudeva